Unsecured loans are a popular financing option for individuals looking to borrow money without putting up collateral. Whether you’re considering taking out a personal loan, consolidating debt, or managing unexpected expenses, understanding unsecured loans is essential to making informed financial decisions.

In this guide, we’ll break down everything you need to know about unsecured loans, including how they work, their benefits and drawbacks, and how to avoid common mistakes. Let’s dive in and explore the world of unsecured loans to see if they’re the right fit for you!

What Is an Unsecured Loan?

An unsecured loan doesn’t require the borrower to provide collateral, such as a car or house, to secure the loan. Instead, these loans are granted based on the borrower’s creditworthiness, often determined by their credit score.

Examples of unsecured loans include personal, student, and credit cards. While they offer the benefit of not risking personal assets, unsecured loans typically come with higher interest rates than secured loans, as lenders assume more risk without collateral.

Legal Consequences of Defaulting on an Unsecured Loan

If a borrower defaults on an unsecured loan, the lender cannot seize specific assets immediately. However, the lender may pursue legal action to recover the debt, which can result in significant financial and legal consequences for the borrower. There are two essential processes to understand: the Stages of Creditors’ Actions for Debt Recovery and the Stages Debtors Go Through Before Bankruptcy.

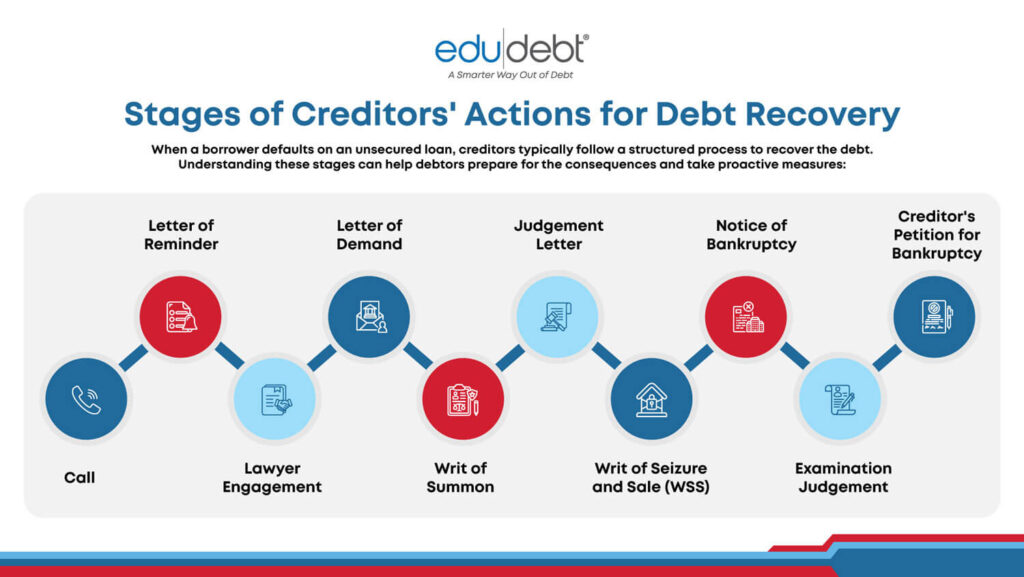

Stages of Creditors’ Actions for Debt Recovery

When a borrower defaults on an unsecured loan, creditors typically follow a structured process to recover the debt. Understanding these stages can help debtors prepare for the consequences and take proactive measures:

- Call

Creditors usually begin by calling the borrower, reminding them of the overdue payment, and urging them to settle the debt. - Letter of Reminder

If phone calls are unsuccessful, the creditor sends a formal reminder letter detailing the overdue amount and requesting immediate payment. - Lawyer Engagement

At this stage, the creditor may engage a lawyer to handle the recovery process, signaling the potential for legal escalation. - Letter of Demand

The creditor’s lawyer sends a demand letter, giving the debtor a final opportunity to settle the debt before initiating legal action. - Writ of Summon

If no settlement is reached, the creditor files a writ of summon in court, starting the formal lawsuit process. - Judgement Letter

Once the court issues a ruling, the debtor receives a judgment letter outlining the obligation to pay the outstanding debt. - Writ of Seizure and Sale (WSS)

If the debtor fails to pay after the judgment, the creditor may obtain a WSS, allowing them to seize and auction the debtor’s assets. - Notice of Bankruptcy

If the debt remains unpaid, the creditor may serve a notice of bankruptcy, warning the debtor of impending bankruptcy proceedings. - Examination Judgement

Sometimes, the court may require the debtor to attend an examination hearing to disclose their financial situation before further enforcement. - Creditor’s Petition for Bankruptcy

Finally, if all else fails, the creditor can file a petition to declare the debtor bankrupt, leading to asset liquidation.

Stages Debtors Go Through Before Bankruptcy

In some cases, unpaid debt can lead to bankruptcy if the borrower cannot repay it even after legal actions like the WSS. Here are the stages that debtors may go through before reaching bankruptcy:

- Default and Demand for Payment

The process starts with the borrower defaulting on their payments and receiving multiple notices from the lender requesting settlement. - Writ of Seizure and Sale (WSS)

If legal action is taken, the lender may obtain a WSS to seize the borrower’s assets for auction, aiming to recover the outstanding debt. - Statutory Demand

If the debt remains unpaid after enforcement actions like the WSS, the lender can issue a statutory demand. This legal notice gives the borrower a fixed period (usually 21 days) to pay the debt. Failure to comply can lead to bankruptcy proceedings. - Bankruptcy Proceedings

If the debt is unresolved after the statutory demand, the lender can file for bankruptcy. This formal legal process liquidates the borrower’s remaining assets to repay creditors, with long-lasting effects on the debtor’s credit and financial future.

Types of Unsecured Loans

Unsecured loans provide flexible borrowing options without the need for collateral. These loans rely on your creditworthiness and offer various solutions tailored to different financial needs. Below, we explore the most common types of unsecured loans available, each designed to help you manage your finances effectively.

Personal Loans

Personal loans are versatile, general-purpose loans provided by banks and licensed moneylenders. They have fixed terms and interest rates, making them ideal for various needs, including home renovations, medical expenses, and vacations.

Banks typically offer more significant loan amounts, extended repayment periods, and more competitive interest rates, suitable for borrowers with good credit histories.

Licensed moneylenders may provide quicker access to smaller amounts with fewer prerequisites, which can benefit those needing immediate funds. With a clear repayment schedule, personal loans offer borrowers predictability and straightforward budgeting, allowing them to plan their finances with certainty.

Credit Card Installment Plans

Credit card installment plans allow you to convert purchases into manageable monthly payments. This option enables you to spread the cost of a large purchase over a fixed period, making it easier to manage your finances without immediately paying off the total amount.

Balance Transfer Plans

Balance transfer plans effectively manage credit card debt by allowing you to transfer outstanding balances to a new credit card with a lower interest rate. This can help reduce the cost of interest payments and make it easier to pay down the debt faster.

Line of Credit

A line of credit is a flexible, unsecured loan with a predetermined credit limit that you can borrow from as needed. Unlike personal loans, you only pay interest on the amount you draw, making it a convenient option for ongoing or unexpected expenses.

Debt Consolidation Plan

A debt consolidation plan is designed to help borrowers manage multiple debts by combining them into a single loan with a lower interest rate. This simplifies the repayment process, often resulting in lower monthly payments and reduced overall interest costs, making debt management more manageable.

How Unsecured Loans Work

Unsecured loans are granted without collateral, relying on the borrower’s creditworthiness, typically indicated by their credit score and financial history. Individuals with higher credit scores are more likely to be approved for unsecured loans and enjoy lower interest rates.

Since no collateral is required, unsecured loans present a higher risk to lenders, often leading to higher interest rates than secured loans. Borrowers should be mindful of the following aspects when applying for unsecured loans:

- Approval Based on Creditworthiness

Lenders assess a borrower’s credit score, income, and financial history to determine their loan repayment ability. A higher credit score increases the chances of approval and often results in better terms. - Fixed or Variable Interest Rates

Unsecured loans may have fixed or variable interest rates. Fixed rates offer predictable monthly payments, while variable rates may fluctuate based on market conditions, potentially increasing costs over time. - Repayment Terms

Unsecured loans typically come with shorter repayment periods, which means higher monthly payments than secured loans. Choosing a loan with a repayment schedule that fits your financial situation is essential. - Consequences of Defaulting

While unsecured loans don’t involve collateral, failure to repay them can still lead to serious financial consequences, including legal action. As discussed earlier, defaulting on an unsecured loan can escalate to lawsuits and enforcement actions like the Writ of Seizure and Sale.

Unsecured Loan vs. Secured Loan

When considering borrowing options, it’s essential to understand the differences between unsecured and secured loans. Both types of loans serve different financial needs and have their terms and conditions. Knowing how they work can help you make informed decisions and choose the loan that best suits your financial situation.

Secured Loans

Secured loans require the borrower to offer collateral, such as a car or house, to secure the loan. This collateral provides a safety net for the lender, reducing their risk if the borrower defaults. As a result, secured loans often come with lower interest rates and more extended repayment periods, making them a popular choice for large purchases like homes or vehicles.

- Require collateral (e.g., car, house).

- Lower interest rates due to reduced lender risk.

- Often used for more significant loan amounts.

- Typically, they have more extended repayment periods.

Unsecured Loans

Unsecured loans do not require collateral, making them a higher risk for lenders. Approval for unsecured loans is usually based on the borrower’s creditworthiness, including their credit score and financial history. These loans often come with higher interest rates and are commonly used for smaller loan amounts with shorter repayment periods, such as personal loans or credit cards.

- No collateral is required.

- Higher interest rates due to increased lender risk.

- Typically used for smaller loan amounts.

- Shorter repayment periods compared to secured loans.

Understanding the Implications of Unsecured Loans

Taking out an unsecured loan comes with specific considerations that borrowers should know before deciding. While these loans can provide quick access to funds without collateral, they often come with higher interest rates and potential risks. Understanding these implications can help you make an informed choice that aligns with your financial goals.

Higher Interest Rates

Unsecured loans generally have higher interest rates than secured loans due to the lack of collateral.

Impact on Credit Score

Defaulting on an unsecured loan can significantly negatively impact your credit score, making it harder to secure loans in the future.

Debt Consolidation

Unsecured loans can be a valuable tool for consolidating multiple debts into one payment, but it’s essential to consider if this is the best option for your financial situation.

Consider Before Deciding

Always carefully consider the potential implications and risks of taking out an unsecured loan to ensure it is the right choice for your financial needs.

Common Mistakes to Avoid

Taking out a loan can be a helpful financial tool, but navigating the process carefully is essential to avoid potential pitfalls. By being aware of common mistakes and taking proactive steps, you can make informed decisions that protect your financial well-being. Below are some common mistakes to watch out for when considering a loan.

Not Reading the Fine Print

Reading and understanding the fine print is crucial when taking out a loan. Overlooking the details regarding terms, interest rates, and fees can lead to unexpected costs and conditions that may not be favorable to you.

Ignoring Financial Impact

Before taking out a loan, consider how it will impact your financial stability and long-term goals. Failing to do so can lead to financial strain and derail your plans.

Not Estimating Disposable Income

A common mistake is not accurately estimating your monthly disposable income to determine what you can afford in loan repayments. This can result in taking on a loan that stretches your finances too thin.

Not Reviewing Terms Before Signing

Review all terms and conditions before finalizing a loan agreement to ensure you fully understand your obligations. Skipping this step can lead to unpleasant surprises later.

Unsecured Loan Features to Consider

When evaluating unsecured loan options, it’s essential to understand the various features that can impact your borrowing experience. These features determine the terms of your loan and affect how manageable and affordable the loan will be over time. Below are some key aspects to consider when choosing an unsecured loan.

Credit Limit

The credit limit is the maximum amount of money you can borrow with an unsecured loan. This limit is typically determined based on your credit score, income, and overall creditworthiness.

Interest Rate

The interest rate is the percentage charged on the loan amount, which determines the cost of borrowing. Unsecured loans often have higher interest rates than secured loans due to the increased risk for lenders.

Curious about how much interest you’ll pay? Use our debt calculator to find out now!

Repayment Period

The repayment period is the time you have to repay the loan. Unsecured loans usually offer shorter repayment periods than secured loans, which can impact the monthly payment amounts.

Fees

Fees are additional charges associated with taking out an unsecured loan. These can include origination fees, late payment fees, and prepayment penalties, which can increase the overall cost of the loan.

Loan Repayment

Loan repayment involves paying back the borrowed amount and any interest and fees. Understanding the repayment schedule and ensuring you can meet the monthly payments is crucial to avoid defaulting on the loan.

Conclusion

Unsecured loans offer a practical solution for managing personal finances, especially when collateral isn’t an option. However, it’s crucial to thoroughly understand the terms and conditions associated with these loans, as they often come with higher interest rates due to the lack of collateral.

Before committing to an unsecured loan, consider the potential implications, including the impact on your credit score and the repayment obligations. By carefully reviewing the tips and guidelines provided, you can make informed decisions and confidently secure an unsecured loan that aligns with your financial goals and needs.

Managing Your Unsecured Loans with EDUdebt

While we don’t offer specific unsecured loan products at EDUdebt, we’re here to assist if you’re navigating the complexities of unsecured loans and aren’t sure which path is right for you. We invite you to take advantage of a free consultation with our experienced consultants, who can guide you through your options and help you find the best approach.

We will assist you in evaluating all applicable unsecured loan solutions and recommend the one that fits your needs.

By working with EDUdebt, you can develop a repayment plan structured around your financial situation, making managing unsecured loans more straightforward and stress-free.

Take the first step towards effectively managing your unsecured loans today. Visit EDUdebt to schedule a complimentary consultation and work towards a more secure financial future. Let us help you turn your financial challenges into manageable solutions tailored to your situation.

Connect with EDUdebt now and take control of your financial destiny!