If your monthly payments feel impossible, your inbox is filled with overdue notices, and you’re losing sleep over money… you’re not alone.

For many working adults, parents, and sole breadwinners in Singapore, unsecured debt can spiral out of control—quietly at first, then all at once. But there is a way out. A debt management plan may be the structured, legal solution you’ve been searching for.

In this article, you’ll learn how to take control of your finances with practical steps on how to start a debt management plan and regain financial stability.

Understanding Debt Management Plans (DMP)

A Debt Management Plan (DMP) is a structured repayment arrangement tailored to your financial situation. It’s designed to help you repay your debts in full—but on terms you can realistically manage. DMPs in Singapore typically cover unsecured debts owed to banks and credit card issuers, and credit card issuers, including consumer banks. These debt repayment programmes are suitable for debtors who have significant amounts of debt with these institutions.

Here’s what a DMP typically involves:

- Reviewing your debts and monthly cash flow with the counsellor, and having your situation assessed by the counsellor

- Negotiating with creditors, such as banks and credit card issuers, for a reduced interest rate or adjusted payment terms

- Consolidating multiple debts into a single monthly repayment submitted to the creditors

If you are a debtor who owes unsecured debts to the above institutions, you may be able to qualify for a DMP if you can make regular payments according to the plan. DMP is one of several debt repayment programmes available in Singapore, and the suitability depends on the type and amount of debt you have.

It’s not a shortcut, and it’s not for everyone—but for many individuals, it’s a lifeline before their financial situation becomes legally or emotionally unmanageable.

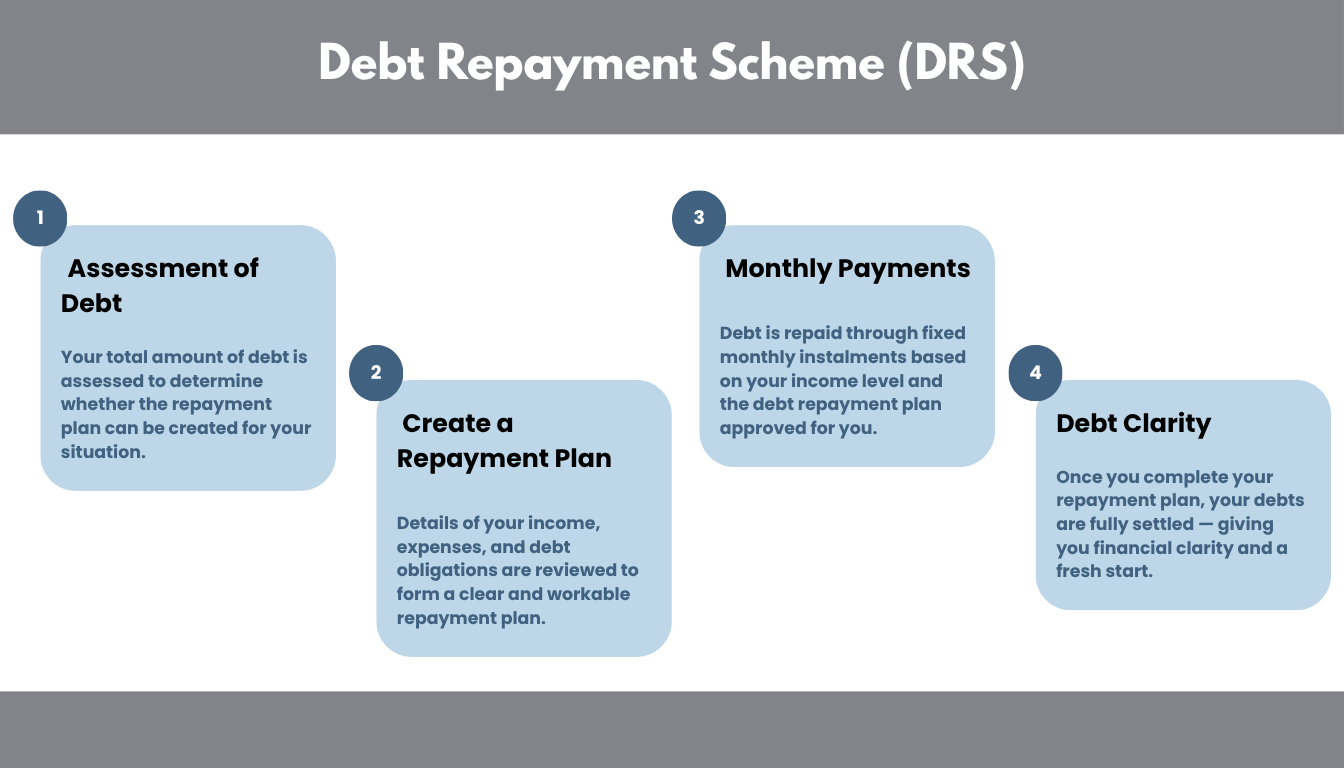

What Is the Debt Repayment Scheme (DRS)?

Separate from general debt management plans, the Debt Repayment Scheme (DRS) is a formal framework governed by Singapore’s legal system.

Key features:

- It’s usually applied to individuals with debts under S$150,000

- The plan can extend up to 5 years

- It allows you to avoid bankruptcy while repaying under the supervision of the Official Assignee

When you are on the DRS, your participation is reported to the credit bureau, and your repayments are made according to the plan approved by the Official Assignee.

To qualify, you’ll need to show that you have a stable source of income and a genuine ability to repay debts within the required time. Your application is submitted to the Official Assignee for assessment.

For many, DRS offers a sense of structure, privacy, and control—without the social and legal consequences of bankruptcy.

Another option is the moneylender debt management programme, a voluntary repayment plan facilitated by CCS specifically for unsecured debts owed to licensed moneylenders. This programme is distinct from DRS and is designed to help debtors manage their obligations to the moneylenders.

Benefits of Structured Debt Repayment

Whether through a DMP or DRS, the benefits of a structured debt plan are both practical and emotional:

- Lower monthly instalments tailored to your income

- Potential interest reduction through creditor negotiation

- One repayment instead of juggling multiple

- Avoidance of late fees and legal action

- Peace of mind knowing there’s a clear, legal path forward

Over time, many individuals find that their anxiety reduces, their budgeting improves, and they regain confidence in managing money.

How a Debt Management Programme (DMP) Typically Works

Here’s a simplified overview of how the process works:

Review Your Financial Situation

A consultant helps assess your debts, income, and expenses. This assessment is conducted by the consultant to determine if you will be able to make the required payments.

Prepare a Repayment Proposal

A proposal is prepared by the consultant and submitted to the creditors. This includes affordable monthly instalments, potential interest rate adjustments, and covers unsecured debts such as credit cards. The proposal is part of broader debt repayment programmes available to debtors in Singapore.

Submit to Creditors

The proposal is submitted to the creditors by the consultant. Approval is not guaranteed but is common when the plan is reasonable and backed by evidence provided to the creditors.

Begin Monthly Repayments

Once accepted, you begin repaying under the agreed terms. When you are on the DMP, your repayments are made according to the negotiated schedule and may benefit from a reduced interest rate. This typically starts soon after approval and continues until debts are cleared.

Stay Committed & Track Progress

Regular reviews are conducted by the consultant to help you adjust as your income or expenses change. Debtors must remain committed to the plan to the end for successful completion.

Managing Debt & Staying on Track

Debt management is not just about repayment—it’s about changing your relationship with money.

Tips to stay on track:

- Maintain emergency savings to avoid new borrowing

- Avoid taking new credit while under a plan

- Use a budgeting tool to track spending and plan ahead

- Reach out for support if you’re falling behind

Many individuals also benefit from financial counselling or money management workshops, which help build stronger habits for life after debt.

Will This Affect My Credit Score?

Yes—but often for the better in the long run.

- Entering a plan may initially affect your access to new credit

- However, consistent repayments reflect positively on your credit behaviour

- Once fully repaid, your progress can help rebuild your credit profile

- Your credit report may reflect the repayment plan, but this is only visible to you and licensed institutions

Think of it not as a step backwards, but as a foundation to build your financial credibility again.

When Should You Seek Help?

If you’re:

- Missing payments month after month

- Taking one loan to pay off another

- Experiencing constant stress from creditors

- Unsure what options are legal, safe, or effective…

Then now is the right time to explore your options. Getting help early means fewer penalties, less emotional strain, and a higher chance of recovery without legal consequences.

Need Someone Who Actually Gets It?

At EDUdebt, we’ve helped countless Singaporeans navigate out of overwhelming debt with confidential, non-judgmental guidance.

We don’t sell promises. We help you find structure, relief, and confidence in your financial life again.

💬 Ready to see your options?

Talk to an EDUdebt consultant today—privately and without pressure.

Your restart begins with a single step.