Struggling with rising balances, missed payments, or cash flow stress? Learn the 5 early warning signs your debt is becoming unmanageable in Singapore.

5 Early Warning Signs Your Debt is Becoming Unmanageable in Singapore

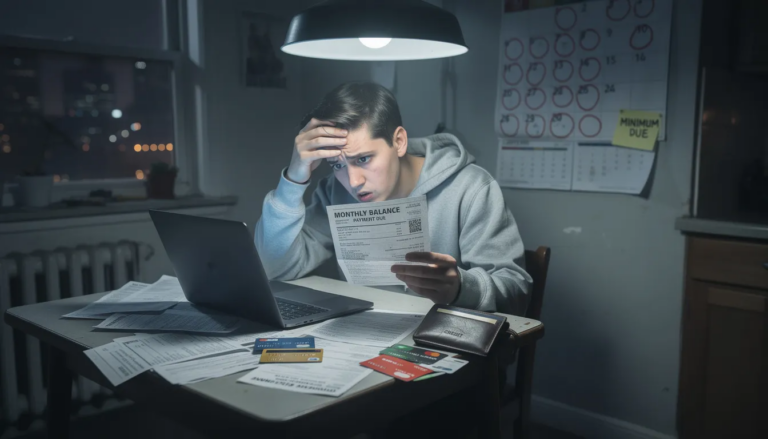

In Singapore, most people don’t realise their debt is becoming unmanageable until something breaks.

A bank suddenly rejects their application.

A credit card limit gets reduced without warning.

Or debt collectors start calling — more often than expected.

By then, options are fewer, stress is higher, and fixing the problem costs far more than it needed to.

The truth is, unmanageable debt rarely starts with missed payments. It starts quietly — through minimum payments, growing balances, and repayment plans that no longer match real-life cash flow.

This article outlines five early warning signs that your debt may be slipping out of control — so you can recognise the problem early and take action before it escalates into serious financial distress.

What Does “Unmanageable Debt” Really Mean?

Unmanageable debt does not mean you missed one loan repayment.

It means your overall debt load has grown beyond your repayment capacity, even if:

- You are still making minimum payments

- Your income has not dropped

- You have not defaulted on any loan agreement

In Singapore, unmanageable debt often involves:

- Multiple unsecured debts such as credit card debt and unsecured loans

- High interest loans with compounding late fees

- Repayment schedules that no longer align with income stability

- Cash flow pressure that affects daily living expenses

When debt becomes unmanageable, it stops being a financial tool and starts harming your financial health and long-term goals.

How Unmanageable Debt Escalates: A Simple Risk Ladder

Not all debt problems carry the same level of urgency.

In practice, unmanageable debt often escalates in stages. Understanding where you fall on this ladder can help you assess how serious your financial situation really is.

Level 1: Minimum Payments With No Progress

You make payments on time, but balances remain high or continue growing due to interest rate structures.

Level 2: Using New Credit to Service Existing Debt

You rely on personal loans, cash advances, or credit facilities to meet existing loan repayment obligations.

Level 3: Debt Repayments Affect Essential Expenses

Loan repayments begin competing with utility bills, groceries, transport, or other necessities.

Level 4: Disrupted or Missed Repayment Schedules

Automatic payments fail, late fees accumulate, and managing multiple loans becomes difficult.

Level 5: Considering Unlicensed or Illegal Lenders

You explore quick cash options from unlicensed money lenders or loan sharks, exposing yourself to severe legal and financial consequences.

If you recognise yourself at Level 3 or above, your debt is no longer just “tight” — it is becoming structurally unmanageable.

Warning Sign #1: You Are Only Making Minimum Payments — and Balances Keep Growing

Many people assume that as long as they pay the minimum payment, their debt is under control.

In reality, this is one of the earliest warning signs of unmanageable debt.

Minimum payments on credit cards mainly cover interest, not principal. With high interest rates, outstanding debts may barely reduce — or even increase — over time.

If your credit card bill looks almost the same every month despite regular payments, your repayment plan is no longer working.

This is how many people quietly fall into a debt trap without realising it.

Warning Sign #2: You Are Using New Loans to Pay Existing Debt

Using one loan to repay another is a major red flag.

Common examples include:

- Taking a personal loan to pay off credit card debt

- Using cash advances to cover loan repayments

- Borrowing to manage unexpected costs or utility bills

While legitimate lenders may still approve you as an eligible borrower, this does not mean your debt remains manageable.

When new debt is used to service existing debt, your overall debt increases — along with interest and hidden fees.

Warning Sign #3: Debt Repayments Are Affecting Basic Living Expenses

When debt repayments start affecting essential expenses, the situation has already escalated.

Early signs include:

- Delaying utility bills

- Cutting essential spending instead of discretionary spending

- Draining savings or emergency funds

- Constant cash flow stress

Healthy repayment plans should support your life, not consume it.

If you are forced to choose between loan repayment and daily necessities, your debt has begun to damage your long-term financial health.

Warning Sign #4: You Are Managing Multiple Loans With Different Terms

Having multiple loans is not automatically a problem — losing track of them is.

This often involves:

- Credit card debt across multiple banks

- Personal or business loans with different interest rates

- Car loans combined with unsecured loans

Different repayment terms increase the risk of missed payments, late fees, and growing debt repayments.

As complexity increases, even previously manageable debt can become unmanageable.

Warning Sign #5: You Are Considering Unlicensed or Illegal Lenders

This is one of the most serious warning signs.

When people start considering unlicensed money lending or illegal lenders, it often means traditional banks and licensed financial institutions are no longer viable options.

Unlicensed lenders typically charge extremely high interest rates and use aggressive collection methods, leading to severe legal consequences and emotional distress.

Once illegal lenders are involved, the situation becomes far harder to resolve.

Why Early Action Matters in Singapore’s Financial System

Singapore’s financial system is structured, regulated, and unforgiving once debt problems escalate.

Financial institutions assess borrowers based on:

- Repayment history

- Existing debt

- Income stability

- Credit bureau records

As debt stress increases, borrowers may face:

- Rejected loan applications

- Reduced access to credit facilities

- Higher interest rates

- Long-term impact on housing, car loans, or business financing

This is why many individuals seek credit counselling in Singapore early — before debt reaches a critical stage.

What You Can Do If You Recognise These Warning Signs

If one or more of these warning signs feels familiar, the goal is not panic — it is clarity.

Practical first steps:

- Stop taking new unsecured loans

- Review your total outstanding debts and repayment amounts

- Create a realistic budget plan based on income and expenses

- Seek professional financial counselling early

Financial counselling helps you understand your financial situation clearly and explore responsible options without worsening your position.

Regaining Control Before Debt Becomes a Crisis

Unmanageable debt does not begin with failure.

It begins when financial circumstances change — but repayment strategies do not.

Recognising early warning signs gives you something many people lose when debt becomes overwhelming: time and choice.

Time to regain control before consequences escalate.

Choice to protect your long-term financial health.

Seeking clarity early is not an admission of defeat.

It is a responsible step toward staying debt free and rebuilding confidence in your financial future.